Mutual funds may seem complicated to people new to investing or investment products. They are a comparatively safer and low-risk investment option. If you have not invested in any form before and have as little as Rs. 5000 to spare, you can start a simple investment option known as “Mutual Funds”.

Mutual Funds are a good option for new investors because of the following advantages:

- Mutual funds are designed to make investing low-cost and straightforward. You can begin investing with as little as Rs. 5,000.

- Investors are not burdened with the decision and research involved in selecting the stocks and bonds to be purchased in the funds or the daily management and safekeeping of the chosen investments.

What are Mutual Funds

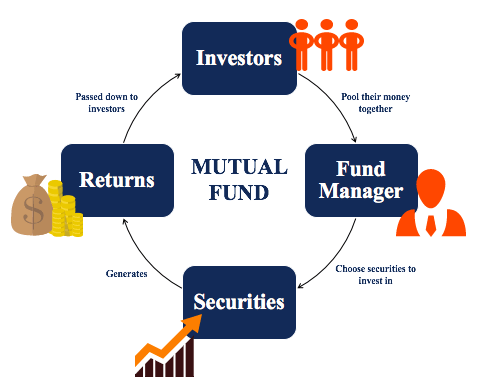

A mutual fund is a selection of stocks, bonds, money market instruments, or any similar assets bought by the investors’ money. A mutual fund can be different combinations of stocks, stocks & bonds, or any other variety of securities combined under the mutual fund as a single investment pool.

This combination is specified in the mandate of the mutual fund, and they cannot deviate from the set mandate.

Mutual fund investments are managed by Money or Fund Managers, who make the investment decisions and manage the funds to ensure that capital gains are maximized for investors.

Mutual funds are run by Asset Management Companies (AMCs), usually public limited companies. A Trust (and Trust Deed) is established by the Asset Management Company under which a mutual fund is launched. The Trustee acts as the custodian of the fund’s assets while the Fund Manager makes the investment and related operational decisions regarding the fund. Asset Management Companies can launch and manage multiple mutual funds with different or overlapping, or entirely distinct mandates.

Why Invest in Mutual Funds:

Mutual funds offer an optimized investment option to yield competitive returns to meet long-term or short-term financial goals. The investor can invest with the long-term financial goals of arranging funds for their child’s higher education or retirement savings or child’s marriage etc. An investor can also have short-term financial goals like saving for a vacation or buying a new car or a new home.

Before investing in mutual funds, all investors need to know their investment objectives. This will help determine the risk and return profile, investment timeline, and target goals. Understanding these questions will allow an investor to make more effective investment decisions.

By investing in mutual funds, the investor gets the advantage of exposure to different securities under a single investment package. They allow the investor to develop a diversified portfolio of assets while enjoying financial management by professionals.

Another key advantage of investing in mutual funds is that the investor can avail tax credit.

Types of Mutual Funds:

There are two primary forms of mutual funds. These are

- Closed-Ended Mutual Fund: These funds are traded on the Secondary Market after their launch through an Initial Public Offering.

- Open-Ended Mutual Funds: These funds are issued in the form of Units to investors, which can be redeemed (sold back) based on their Net Asset Value (NAV) at any time. These funds can be purchased and redeemed through the Fund Management Company, which daily announces their offer and redemption prices. These funds can also be listed on the Stock Market.

Categories of Mutual Funds:

Mutual Funds are of different categories. These categories are based on where the fund invests, its risk profile, and the investment strategy. In Pakistan, the following mutual fund categories are approved by the SECP.

1. Money Market Fund

These funds invest in short-term fixed-income securities like government bonds and certificates of deposits, and commercial paper. Their aim is to maintain high liquidity by investing in low-risk instruments that are generally safer.

2. Income Fund

These funds generally invest in market securities, term finance certificates/sukuks, commercial paper, and spread transactions. They aim to generate a regular stream of income for their unitholders.

An income fund is generally seen as less risky compared to an equity fund as it is not likely to be affected by market volatility. The probability of capital appreciation is also limited.

3. Equity Fund

These funds invest in stocks and grow faster than money market or fixed-income funds. This means they carry a higher risk as they are exposed to market volatility. An equity fund aims to provide exposure to listed equity securities and capital appreciation over the medium to long term.

4. Balanced Fund

A balanced fund offers exposure to both growth and regular income by investing in equities and fixed income securities. Regulations require that balanced funds keep 30% to 70% of their net investments in listed equity securities.

The other remaining can be invested in other certified investments. Balanced funds are exposed to both risks of fluctuations in equity markets and interest rate variations. Balanced funds can be risky like equity funds but are less risky than equity funds based on asset allocation.

5. Asset Allocation Fund

These funds can invest in any type of securities subject to conditions to diversify their assets across different types of securities and investment styles as written in their offering document. Asset allocation funds are generally considered high-risk funds due to their potential to be fully invested in equities at any point in time.

6. Capital Protected Fund

This type of fund makes investments in such a way that the original amount of investment is safe to ensure positive investment returns. This fund keeps a significant part of its net amount in a bank in the form of a term deposit. At the same time, the remaining is invested in accordance with the authorized investments stated in the offering document. Unlike other funds, the capital-protected fund has a fixed maturity period specified under the investment period or tenure.

7. Index Tracker Fund

This type of fund is designed to carry out the activities of a particular index and show the probable tracking in the offering document. Investment of at least 85% of net assets is required in the securities that constitute the selected index or subset.

8. Fund of Funds

This fund holds other mutual funds in its portfolio rather than investing directly in any security. However, each fund of funds will have its own category, for instance, equity fund of funds, income fund of funds, etc.

An investor can invest in the fund that suits his investment strategy, the investment time horizon, how much risk he can tolerate, his cash flow requirements, or any other investment objectives/ requirements.

The Mutual Funds Association of Pakistan has a very helpful website http://www.mufap.com/ with comprehensive details and comparisons of fund performance.

Key Terms:

Some key terms used in mutual funds investment that you should know are as follows:

Net Asset Value (NAV):

Net Asset Value is the market value of a mutual fund’s assets after deducting its expenses and liabilities on a particular day. The per unit NAV is the Net Asset Value of the funds divided by the number of units/ certificates outstanding on the Valuation Date. The NAV shows the performance of a mutual fund.

NAV = (Current Market Value of all Assets – Expenses – Liabilities) / (Total Number of Units Outstanding)

Expense Ratio:

Expense Ratio is the fund’s annual fund operating expenses, expressed as a percentage of its average net assets. An Expense Ratio of 1% p.a. means that 1% of the fund’s total assets will be used to cover expenses each year. Expense Ratios are essential to consider when choosing a category of mutual fund as they can significantly affect returns.

Redemption:

The units of open-end mutual funds can be partially or fully redeemed at any time from the Asset Management Company that manages the funds.

Fund Manager Report

This is a monthly report produced by an asset management company in which information on the composition and performance of the mutual funds is presented.

How to Invest in Mutual Funds:

The documents needed for opening a mutual fund account are as follows:

- CNIC Copy

- Application/ Account Opening Form/ Purchase of Units Form

- Zakat Affidavit (Optional)

- KYC Form/ FATCA Form

- Cheque/ Pay Order/ Demand Draft (payable to the respective Trustee)

Fees & Charges:

You must keep in mind that there are charges involved with investing in mutual funds. Some of these charges are as follows:

- One-time Fee: This fee is paid for investment/ divestment in an open-end fund. Details of these fees are disclosed in the offering documents.

- Front-end Load: This is charged on the purchase of units of the fund.

- Back–end Load: This is charged when an investor redeems his investment in the mutual fund.

- Contingent or Deferred Sales Load: This is charged only when there is no front-end load. This load ischarged on redemption of investment. However, funds can reduce it progressively if an investor holds an investment for a more extended period.

- Management Fee: This is the fee charged by the AMC for the management of a fund.

- Trustee Fee: This is the fee charged by the Trustee to provide trusteeship and other services for the fund’s assets.

Benefits Of Investing In Mutual Funds:

Asset management companies manage mutual funds. They evaluate investment opportunities by researching, selecting, and monitoring the performance of the securities purchased by the fund. These tasks are done by qualified financial professionals who make calculated investment decisions on your behalf.

Diversification

A mutual fund can help reduce investment risk if a company or sector fails by spreading its investments over other securities and investment sectors.

Affordability

Mutual funds are ideal for investors without a lot of money to invest. They have relatively low Rupee amounts for initial purchases and subsequent monthly purchases. For example, you can add funds at set amounts of, say, PKR 1,000 to 5,000 per month or other intervals. This is not difficult to set aside for savings or investment purposes.

Liquidity

Mutual fund unit holders can easily redeem their units into cash on any working day. They will receive the applicable value (NAV) of their investment within six working days. Investors do not need to look or wait for a buyer. The fund buys back (redeems) the units at the current net asset value (NAV).

Well regulated

The SECP continuously monitors all mutual funds through reports that the mutual funds are required to file with the SECP regularly.

Transparency

a mutual fund’s performance is reviewed by different publications, rating agencies, and the SECP. This makes it convenient for investors to compare the performances of different funds. Unit holders also receive regular updates, like daily NAVs, fund’s holdings, and the fund manager’s monthly strategy report.

Tax benefits

Investment in mutual fund schemes entitles the investor to avail tax credit that enhances the overall return on their savings

Things to Know Before Investing In A Mutual Fund

Before selecting an appropriate mutual fund for your savings, you must identify your investment objectives. Your financial goals are determined by your income, expenses, financial independence, age, lifestyle, family stage, etc.

Here are some questions that you should ask yourself and likely answers that will help you select an appropriate mutual fund.

- Why am I investing?

I need some side income, need to save up to buy a home, fund a wedding, save for higher education, or a combination of all these needs.

- What is my risk tolerance?

I am unwilling to take any risk, or I accept that to earn long-term gains, I may book short-term losses.

- What are my cash flow requirements?

I want to multiply my assets for the future and do not need periodic cash flow; I need a regular cash flow, or I need X amount to meet a need in X years.

- What is my time horizon?

- I need some money in under a year (short term), or one to five years (medium-term), or five years or more (long time)

If you answer these questions honestly, you will have clarity of what to expect from your investment.

This will help you determine an appropriate mutual fund investment strategy.

Sadia Zaheer holds a Masters in Business Administration from IBA, Karachi. After working in several financial institutions in Client Management, Corporate Lending, Islamic Banking and Product Management she jumped careers to pursue a career in writing.

She is a Finance, Business and HR Development writer with four years of experience. She reads a lot and takes care of her multiple cats to remain calm.