Retirement planning is a conscious and lifelong process that needs years of commitment. This time is needed to build up sufficient retirement funds for a comfortable and independent retirement. While it is not possible to cover all aspects of early retirement, I hope that the information below will give you a basic understanding of what early retirement requires and how you can plan for it.

Retirement Planning

A conversation with most working professionals will show that many of us dream of retirement and leaving the 9 to 5 life behind us. We all aspire for a happy and relaxed retired life and many of us are willing to plan for it.

Retirement goals are fairly standard and most working professionals have some form of retirement plan. This can be supported by the workplace or can be independent of whatever the workplace retirement plans are. However, what we all need to bear in mind is that real-life retirement can turn out to be very different from what most of us imagined.

The reality checks most retirees face are due to poor financial management and a lack of investment planning. While there are a lot of retirement plans available in the market, having one and relying on it exclusively is not a good plan.

Many other factors will impact your retired life and how it treats you.

Factors to Consider For Retirement

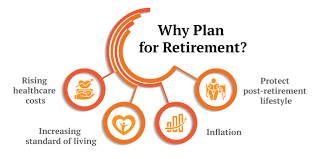

A serene retired life is dependent on 3 major elements, the retiree’s social life, financial condition, and age. Retiring early with a strong financial position, and a good social circle is an ideal goal.

How can we go about achieving this?

1. Financial Stability

To plan for retiring in a stable position, there is a need for a strong financial retirement plan. There are many suitable retirement insurance plans in Pakistan designed to help you retire with ease. However, you need to choose your plans wisely. Bear in mind that even the best retirement insurance plans in Pakistan will not be enough to cover all your financial requirements by the time you are ready to retire.

The factor of inflation is something that cannot be included in the most comprehensive retirement or investment plans. This is something that can be planned out through a customized plan built with a financial consultant. As a base rule, the most comprehensive plan should include some investment in shares and other assets. Out of the proportion of stocks, some should be dividend stocks, and others should be growth stocks.

2. Social Life

Social life is not fully controllable, but something that can be controlled to some extent. People planning for early retirement need to have a social life to rely on once they are free from the 9 to 5 routine and have an idle life. There will be an increased need for meaningful interactions. These need to be cultivated way before the retired life is expected to start. In most cases, we cannot control the people we retire with but if we have time. So, by cultivating meaningful friendships before you retire, you’ll have a better social life when you finally call it quits.

Another perspective of social life is charity or social work. Social work and charity add perspective as well a social perspective to anyone’s life. Social and charitable endeavours help add busyness They also have a bigger friend circle and stay busy doing things that interest them during retirement.

It is a good idea to start by doing volunteer work in orphanages or part-time tutoring to practice giving back to those less privileged. Investing time in such endeavours will pay off in the long run and help an alternate social life to keep yourself occupied after retirement.

3. Retirement Age

The age at which a person retires plays a significant role in how rewarding they find their retirement. 60 is the average age for retirement, but this can vary from person to person. For the very ambitious, the retirement age can be settled anywhere in the late 40s to 50s. this much younger age is set for those that are certain to save up enough to have a settled, happy retired life.

If you prefer to stay busy, you may extend your retirement age by retiring later to enjoy work for longer. Having an alternate lifestyle ready to keep you busy is a good option and necessary to plan a life post-retirement.

Bear in mind that the majority of financially stable retirees aren’t necessarily rich, and not all of them are in high-paying jobs. However, these are people that know how to manage finances and create a comprehensive plan to retire happily.

How to Prepare for a Retired Life

If you’re financially covered with the best retirement insurance plans in Pakistan, then half of your worries will already be covered. However, you’ll have to consider a few other factors when you retire. These include:

Plan to Have Adequate Health Insurance

Health insurance is an absolute necessity for retirees. This is not to say that it is not essential at a young age. But as age increases and health issues increase, the importance of adequate health insurance is highlighted. This is essential, as by investing in a reliable health insurance plan, retirees are always prepared for any health-related emergency costs.

Ensure that Loans and Outstanding Assets are Paid for

This may sound easy but is very hard to implement. However, living with interest obligations, particularly without a regular income stream can be very challenging. If you have to spend a large proportion of your retirement income to pay off debt, there will be little enjoyment in retirement. It is advisable to finish your debt-based obligations and only retire once major loans are paid off.

Plan on How to Spend your Time

The busier a person remains during retirement, the fewer things they have to worry about. Plan about what you will do and design a schedule of weekly or monthly activities. Also, make a to-do list to help constructively spend your retirement time.

The more well planned your retirement, the better it will go. Invest in the best investment plans for retirement in Pakistan, plan on what you’ll do after retirement, and cultivate a strong social circle to keep you company for a fuller, happier retirement.

How to Make a Retirement Plan?

Retirement planning involves setting goals for your retirement and assessing the actions and decisions needed to achieve those goals. It includes settling on sources of income, forecasting expenses and cash flows, how to plan a savings and asset management plan.

For most people living in Pakistan, who do not plan for their retirement, retirement is a stage of life that is defined by:

- Limited income

- Difficulty in managing basic living expenses

- Reliance on children

- Healthcare issues with related expenses

- Living with hardships

- No enjoyment.

For retiring individuals that do not have adequate income for their retired life, living with support from family members can be difficult as well as humiliating. In Pakistan, most private employees are not part of any retirement plan. Private employees have to depend on the next generation to support their old age. In addition, they can rely on rental income from property and interest on bank deposits.

In Pakistan, there is an option for some coverage through retirement benefit schemes that provide lump-sum amounts through provident and gratuity schemes. However, the utility of lump-sum benefits is limited, as they pass on the responsibility of managing these funds to retirees. Pension schemes exist but are mainly for the public sector employees like government and multinationals.

Voluntary Pension Schemes

To facilitate employed and self-employed people to plan for their retirement in a regulated environment, the Securities and Exchange Commission of Pakistan (SECP) launched the Voluntary Pension System (VPS) in 2005. The Voluntary Pension System is regulated by SECP.

- Pakistani nationals above the age of 18 years with a valid Computerized National Identity Card (CNIC) or National Identity Card for Overseas Pakistanis (NICOP) are eligible to participate in VPS.

- Under the VPS, the employee, the employer (or both) can pay in funds to the employee’s pension account (IPA) which is invested for the long term. Contributions can be in a lump sum or at a regular frequency. There is no penalty for missing any payment.

- The pension fund manager issues an individual pension account (IPA) in the individual’s name, who is referred to as a “Participant”. Each pension account (IPA) has a unique identification number (UIN). The funds that are saved up are used to payout a regular pension or lump sum on retirement.

- To protect account holders of these pension funds, the SECP has specified an investment and allocation policy for pension funds setting out the parameters for the investment of payments

- Individuals can distribute their contributions between equities, debt, money market instruments, and commodities. This distribution is by the investor preference and risk appetite.

How to Start Saving for Retirement?

Some key points to note are:

- Analyze income and expenses and make sure that you can save more than you earn.

- Make a budget that includes a specific percentage of savings and follow

- Make sure that you do not take out money from your retirement savings account for emergencies. Has money been set aside for emergencies like job loss, accidents, and medical expenses?

- Open an individual pension account (IPA) from any asset management company, or pension fund manager that you choose. This is the easiest way to start saving for your retirement. Contact information can be found at the following link: http://mufap.com.pk/members.php

- If your employer has a voluntary pension scheme, participate in it.

- Bear in mind that contributions to any voluntary pension scheme in a year are eligible for tax credits.

- Consult investment advisors to select investment products suited for your needs. The present age and expected age of retirement are important for developing an effective retirement strategy. The longer the period to retirement, the higher the level of risk you can tolerate in your portfolio. By investing in stocks, you become partial owners of the company and can participate in earnings as well as losses. Your longer time horizon will allow you to ride volatility in the market and balance your portfolio.

Building your Retirement Fund

You must keep your expectations about post-retirement expenses realistic. While income will decrease, expenses are going to increase over the long term. Most people claim that their annual spending will reduce to 70% of what they spent while working. Such an assumption is often unrealistic, especially if medical expenses are not included in the assumptions.

Always seek financial advice from a trusted financial adviser. Financial professionals can help you design a savings plan appropriate for your particular situation.

Make a habit of saving regularly and try to increase the amount you save each year, this increase should preferably be more than the rate of inflation.

Focus on the long term, do not be concerned about the short-term performance of the investment portfolio. Keep to a long-term plan and review your portfolio periodically to stay on track.

Use a broadly diversified portfolio of stocks and fixed income securities /bonds. The mix of the number of stocks versus fixed income securities /bonds depends, in part on your age, time to retirement, and your ability to tolerate market turbulence or risk.

In short, retiring early can be practical, provided that t is planned for efficiently and over the long term.

Sadia Zaheer holds a Masters in Business Administration from IBA, Karachi. After working in several financial institutions in Client Management, Corporate Lending, Islamic Banking and Product Management she jumped careers to pursue a career in writing.

She is a Finance, Business and HR Development writer with four years of experience. She reads a lot and takes care of her multiple cats to remain calm.