Investing in a high-inflation environment requires a different approach than what you would use in a low-inflation or deflationary environment. To protect your portfolio and potentially even capitalize on inflation, here are some strategies to consider:

1. Diversification

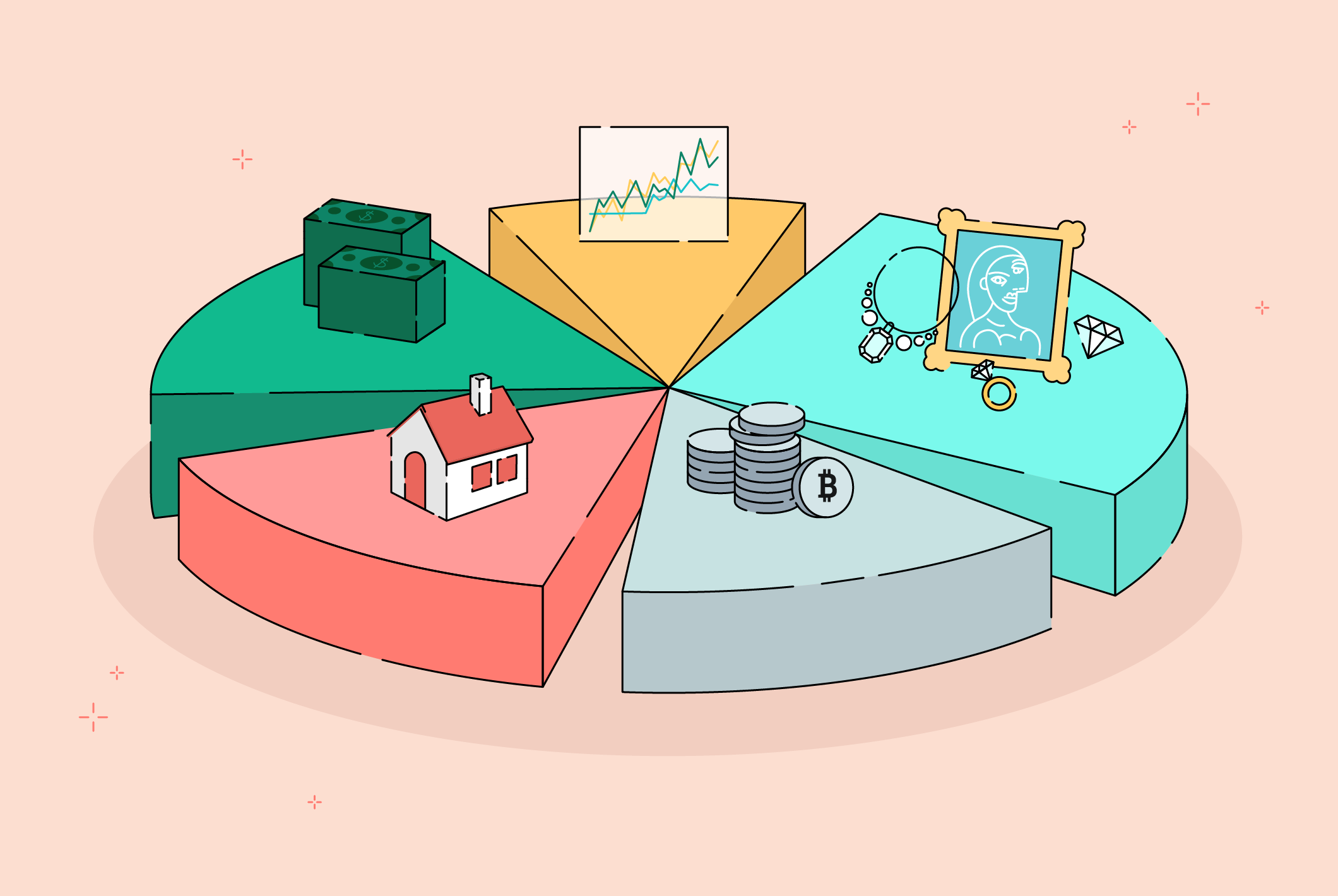

Adding some inflation-resistant diversifiers to your investment portfolio can help reduce the impact of inflation. Inflation-resistant assets are investments that usually maintain or even rise in value during inflationary periods. Such assets include commodities like gold, real estate, inflation-linked bonds, and dividend-paying stocks.

By including these assets in your portfolio, you can theoretically balance the negative effects of inflation and maintain, if not increase, the value of your investments over the inflationary period. The goal of diversification is to reduce overall risk. Adding some more inflation-resistant assets to your portfolio can be a sound strategy for achieving this objective.

Some basic assets to diversify into are:

· Real Estate

Real estate is traditionally known to be a good hedge against inflation as it tends to maintain or even rise in value during periods of inflation. Many real estate assets, such as rental properties, generate income through rent payments.

Rental income usually rises along with inflation. In addition, as the cost of goods and services rises due to inflation, the replacement cost of real estate also tends to increase, which pushes up property values over time. This means that your investment remains secure during inflationary periods.

· Commodities

Investing in commodities is another good way to hedge against inflation since the prices of common commodities like gold, silver, and oil usually rise during inflationary periods. This rise usually occurs because these commodities are seen as better stores of value. They offer adequate protection against the erosion of purchasing power that inflation causes.

-

Dividend-paying stocks

Blue chip stocks that are regular dividend payers can be a good hedge against inflation. Most companies only pay dividends when they have stable cash flows. Such companies can usually sustain and even increase their dividend payouts over time, which can help offset the impact of inflation on your portfolio.

When companies pay dividends, they return a portion of their profits to shareholders. This is seen as a sign of financial strength and stability, which is especially important during inflation when the prices of goods and services are rising. Additionally, dividend-paying stocks offer a regular income stream that can help supplement other income sources, such as a pension.

It is important to note that not all dividend-paying stocks are the same equal, and investors should do their due diligence to ensure that they invest in quality companies with sustainable dividend policies. Investors should also focus on diversifying their portfolios over different sectors and industries to reduce the overall risk of their investment portfolio.

2. Manage your budget

When prices rise, our non-essential spending usually takes the biggest hit as consumers try to cut back on nonessential purchases. Such changes in consumer behavior can play a significant role in reducing the impact of inflation. To adapt to the prevailing market conditions, it usually makes sense to delay buying goods that are heavily impacted by inflation. Assets like cars, furniture, or high-end groceries like meat and mithai (sweetmeat) experience lower demands as users try to manage their limited budget to adjust for higher prices.

3. Don’t Keep your savings in cash

During market turbulence and rising inflation, it may seem safer to withdraw your funds from the market and shift your investments into cash. However, in an inflationary climate, holding onto cash can prove to be harmful.

While it may seem secure since the balance in your account remains constant, it is better to go bargain hunting in a fallen market and pick up strong stocks at lower prices. This allows you to book gains once the stock market recovers and allows you to keep your capital safe as well.

4. Reassess your emergency fund

Most investors decide to keep a larger cash amount in their emergency fund to adjust for the rising expenses that come with inflation. When the cost of goods and services is rising, increasing the size of your emergency fund can offer an added layer of security. It also helps to cover for any unforeseen expenses.

Setting aside enough cash to cover three to six months’ living expenses is normally advised. However, this fund should reflect the current prices during economically uncertain times. You can also revise both prices and the number of months’ budget you keep in your emergency fund. Both strategies are advisable in case of an unexpected financial setback.

5. Reduce your Taxes

It is important to lessen the burden of taxes on your finances, especially in the light of growing taxes. It is necessary to focus on tax efficiency. Investors need to move their tax-inefficient investments into tax-deferred or tax-exempt options, especially during periods of market volatility. This can help in reducing your overall tax burden. By doing so, you may be able to offset the impact of inflation to some extent and ultimately improve your financial standing.

Adopting a defensive approach or investing heavily in short-term assets such as cash and CDs could be exceptionally precarious in the current economic climate. Although we are told to expect a decrease in inflation from its recent highs, it seems likely to take several quarters for this to materialize. Even though there is considerable uncertainty in the investment landscape, exercising excessive caution may pose a genuine threat of eroding the value of your assets over time.

Conclusion

It is important to note that while these strategies may help protect your portfolio in a high-inflation environment, there are no guarantees in investing. As with any investment, it’s important to research, consult a financial advisor, and make decisions based on your financial situation and risk tolerance.

Sadia Zaheer holds a Masters in Business Administration from IBA, Karachi. After working in several financial institutions in Client Management, Corporate Lending, Islamic Banking and Product Management she jumped careers to pursue a career in writing.

She is a Finance, Business and HR Development writer with four years of experience. She reads a lot and takes care of her multiple cats to remain calm.