Most adult Pakistanis living in urban cities work daily and earn an appropriate amount of money. At the end of every month, many usually have empty wallets and emptier bank accounts.

This is particularly true with the growing inflation that makes money fly out of our wallets. Inflation rose to 11.5 percent in November 2021, compared to about 9 percent in October.

This state of being broke at the end of the month is not the norm, and it can be avoided by having some discipline in your spending patterns. To do this, sit down and acknowledge that you have a problem. Once you do this, you are ready to build your budget around your income.

Budgeting is the basis of every savings plan. Whether you earn six figures or live paycheck to paycheck, you are likely wasting money somewhere you shouldn’t be if you don’t budget your income. Unlike the common misconception of pinching expenses and not doing anything fun, budgeting is just a process of keeping track of your income and going.

You can download many of the free budgeting apps available online for free to plan your budgeting campaign.

Words of caution, getting your spending habits on track and following the budget pattern can take time. You will have to follow it and keep following it regardless of failing initially.

Ignore the fails and keep on following your plans to achieve financial success. There is a step-wise process that you can follow to financial independence.

Steps to Financial Freedom in Pakistan

1. Set quantifiable financial goals

These are not the ‘mein bara aadmi banoon ga’ type of goals we all have as kids. This step is about consciously setting aside a fixed amount of money and giving up on some of your unnecessary spending to achieve it.

The amount should be realistic and possible to do. For instance, if you earn PKR 70,000 per month, saving PKR 20,000 may be difficult now if you are running a 4-member household with no other income.

Your goal should be achievable and realistic. Maybe try to save 10,000 but be prepared that a maximum of 5,000 may be used up in emergencies and month end money crunches.

The more detailed this goal is, the more possible it will be to work (and save) towards it. Break your goal into numbers to see how much you need to get there.

2. Split up your income into different bank accounts

Now that you have set a goal to save up a fixed amount every month, you should invest in opening two different accounts.

You already have a salary account to pay your bills, utilities and draw money. If you don’t get paid through bank transfers, open an account ASAP to deposit your salary as soon as you get it.

Having different buckets, or in this case, accounts, to keep your cash in will help to follow a financial plan.

You need to have separate accounts for the following purposes:

1. An account for your daily and fixed monthly expenses. This can be your salary account if you have one. Ideally, this account should have good online banking services and an efficient ATM network. It should also allow for automated monthly transfers.

2. An account for your savings. This should ideally be one WITHOUT any ATM or online banking support for withdrawals. You can have your savings amount directly debited via automatic transfer from your salary account.

The next account may seem to be a little extra, but it is for those who have multiple goals to save up for and don’t know how to prioritize or want to have different heads to organize their savings:

3. An account for your savings. Ideally, this should also be without any ATM or online banking support for withdrawals. You should be able to automate the savings amount transfer from your salary account. If you want to save up for a car or your kids’ higher education, or a house, have separate accounts for these heads setup.

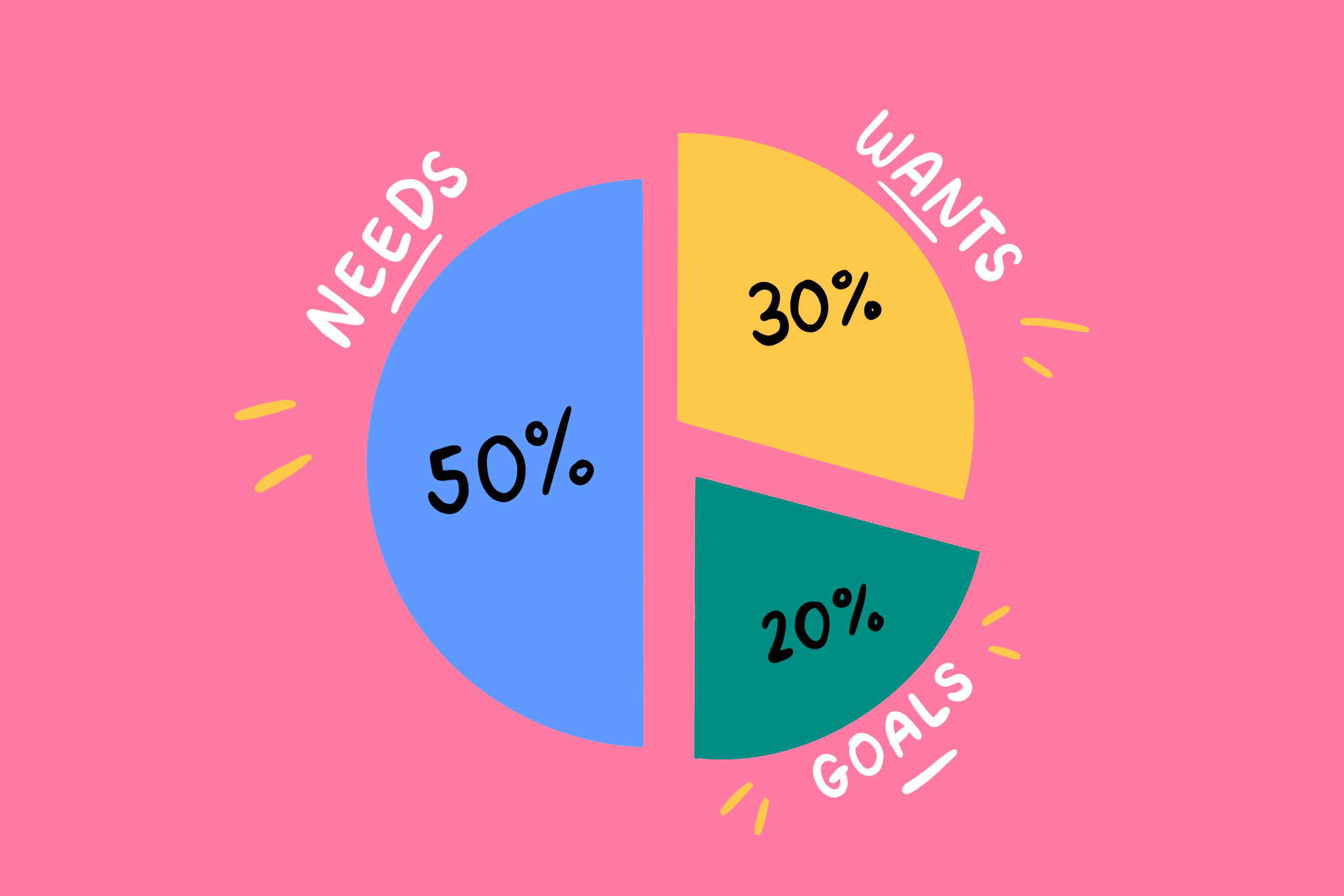

3. Budget your spending to less than 50% on necessities

![]()

Now that you are clear about your goals and what you want to do with what you save, it’s time to deal with the practical stuff. If your take-home salary is Rs. 50,000, try to restrict your spending to PKR 25,000 on necessities.

A well-made financial plan can help you keep track of your spending habits and help you identify where your cash is going. Documenting all spending heads can expose areas where you are spending more than you should. Maybe you spend more on groceries because you go somewhere that charges more. A budgeting exercise would help you identify where you free up additional cash.

Now necessities are the groceries, utilities and rent that you pay. If your take home pay is Rs. 50,000, living in a rented place of PKR. 25,000 doesn’t make sense unless you share rent with others and save on commuting expenses.

Similarly, lunching out regularly or fancy coffees from expensive cafes do not make economic sense. If you have children, their school fees and van expenses are necessities. Outings to Sindbad and fancy tablets do not count as necessities no matter how much social media tells you otherwise.

Keeping to this 50% necessities rule means 50% of your earnings on savings and non-essentials.

4. Limit non-essentials to 20% of your income

Keep 30% of your income for savings and investments. At the same time, the balance of 20% should be used for hobbies, non-essentials like clothes, shopping, and entertainment.

The challenge here would be restricting yourself to stay within the 20% amount you get each month. This amount can be spent on high end clothes, tech gadgets or saved up for a vacation abroad, and it is entirely up to you. All you must focus on is to stay within the budget of PKR 10,000 (20% of Rs. 50,000).

Now, supposing you want to travel to Dubai, you will need to save at least Rs. 100,000 for your trip. This means that you must put aside some money from your 10,000 a month to save up for this holiday.

5. Save the remaining 30% by investing in high return accounts and investment options

Those who continued to get a paycheck during the lockdown in 2020 and 2021 are extremely lucky. Those that were laid off and had to rely on their savings would know just how important it is to have a sizable amount saved up for emergencies.

Ideally, this 30% of 50,000 (PKR 15,000) should be saved up in a high return savings account or other investment options like mutual funds, stocks or insurance policies. All options should be such that withdrawal can be possible at a week’s notice. Deposit interest rates in 2020 were 7.47%. The same deposit will earn you over 11% if placed in Defense Savings Certificates as of December 2021.

The charm of this is that you can diversify your savings into multiple heads. A fixed deposit for emergencies, a savings plan for children’s education or marriage, your marriage, and another long-term plan for retirement or health emergencies like disability.

-

The emergency fund

The emergency fund can be used to save up money to get enough to make a down payment on an insurance policy, car, or even a home. This is also your backup funds in case of job loss, or medical emergency, or any other unexpected sudden expense like a microwave burnout or UPS battery replacement.

A basic rule to follow is to have 6 months’ salary or living expenses always saved up in this account. Anything over that can be placed in short-term investments. If you are in a stable and well-paying job that will give you a severance package if they fire you, keep up to 3 months’ salary in this account and invest the rest.

-

Insurance or savings plan

If you get medical coverage from your employer, count yourself lucky. If you don’t get coverage from your employer, you need to invest in good medical insurance to cover medical consultations, investigations, and procedures.

Getting insurance is particularly important if you have dependents like your parents or children. Take a policy that offers payouts to dependents on your death or yourself in case of a disability or health issue that stops you from working.

Deciding on an insurance policy will require research into mixing and matching policies. You can visit our insurance guides or book an appointment for our insurance advisors to guide you on your insurance plan.

-

Investments

Investing in higher return plans for long-term and retirement goals is a smart financial decision to make. You can opt for stocks, property, unit trusts and savings certificates.

Starting this early and saving up a little every month is key to keeping your investment growing. Compounding will do the rest for you.

Final Advice

According to the break-up detailed above, you can manage your money well by following the 50-20-30 rule. The rule is a standard for savings globally and should stand by you well.

In the case of dual-income households, the rule should apply to both incomes, or break up should focus on more savings and less spending on luxuries. Having more income will mean that you can save up more and have an effective savings plan lined up for your future wellbeing.

Sadia Zaheer holds a Masters in Business Administration from IBA, Karachi. After working in several financial institutions in Client Management, Corporate Lending, Islamic Banking and Product Management she jumped careers to pursue a career in writing.

She is a Finance, Business and HR Development writer with four years of experience. She reads a lot and takes care of her multiple cats to remain calm.