“Both the Quran and hadith inform Shariah, which guides Muslims through practical life decisions”

Including how they should make and save money while remaining true to their religious principles. Saving for retirement the Muslim way involves “very intentional investing that is consistent with values”

The philosophy behind Islamic saving and investing can be traced to the Quran and other early Islamic texts. The story of the prophet Yusuf conserving grain from rich harvests in Egypt, related in Sura (chapter) 12 of the Quran, is often cited as an admonition to save against hard times. Other verses advise against squandering wealth, while the Prophet Muhammad warned in a hadith (a collection of his sayings) that one “who is prudent in spending will not be dependent on others” later in life.

Importance of Planning for Retirement

There are two components to retirement income planning: Personal Planning and Financial Planning. Personal planning is important because it is the determining factor of your satisfaction with your retirement lifestyle.

Financial planning is crucial because it identifies your sources of income and expenses and establishes your retirement budget, based on your plan.

Personal Planning

All too often people entering retirement do not place enough emphasis on personal planning to ensure they maximize their opportunities. So one needs to think well before time and take the time now at an early stage in your planning process to plan and think about your life, to think about the choices you have about how you would like to spend your time during retirement.

What do you think would you pursue when you won’t have the obligations and responsibilities you have today. Do you want to volunteer at a local hospital? Take up that hobby you were always interested in, but never had the time to start? Go back to school and pick up a few special interest courses? Start your own business? Travel around the world? Buy property in a warmer climate and spend the winter months there?

These and many other lifestyle questions based on your preferences are all important factors to consider when planning your retirement since your choices will drive the financial circumstances that must be met to achieve your goals.

Financial Planning

Financial planning is the foundation of all the other planning you wish to take up when you retire, as your finances lead up to the material benefits in the future.

Will you have adequate funds to provide the kind of retirement lifestyle you envision? Remember your income will likely come from three general sources: government pensions, employment-related sources, and your investments.

Your retirement will be more enjoyable if your income is structured to fit your lifestyle choices and if you have developed a retirement plan to protect the assets you have worked hard to acquire.

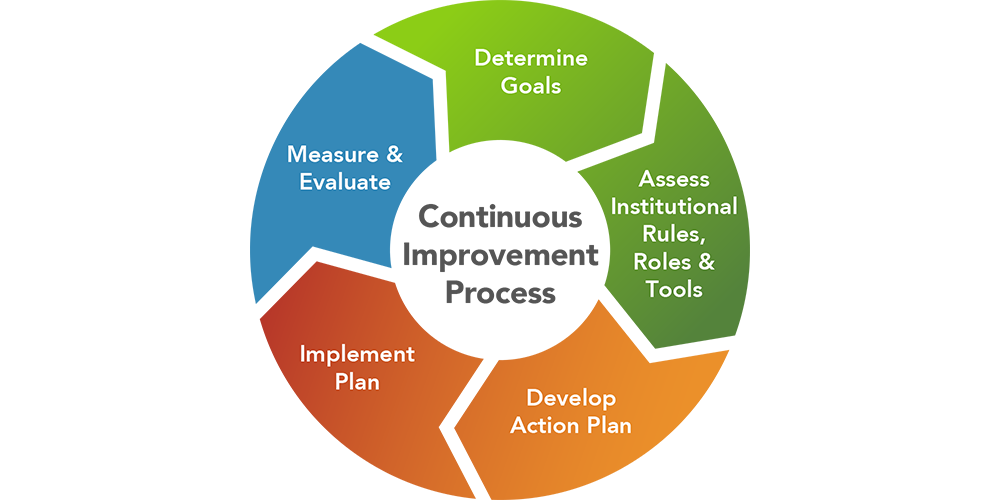

Develop an Action Plan

The concept of retirement has evolved greatly over the last fifty years. If we live longer, we do perhaps retire earlier. Fewer of us have pensions and we are increasingly responsible for providing our income in retirement, a period of our lives that may well last twenty to thirty years.

As you approach the end of your working career, you may have questions about how to support yourself in retirement. How do you know what you’ll need to live on? Which pension option should you select? When should you start collecting Social Security? How will you pay for health care?

Things/factors to keep in mind well before your retirement:

- Set your retirement goals

- Assess your current financial position

- Identifying retirement income sources

- Evaluate your retirement risks

- Understand health care issues

- Invest the retirement assets that you have saved during your working years

- Manage your retirement income

- Monitor your retirement assets

Here are some details for each step:

“Inflation is like an acorn. It starts small, but given enough time can turn into a mighty oak tree”.

We’ve all heard—and want—compound and reliable growth on our money and the sources we plan to invest into. Well, inflation is like ‘compound anti-growth,’ as it erodes the value of your money. A seemingly small inflation rate of 3% will erode the value of your savings by 50% over approximately 24 years.

It doesn’t seem like much each year and may seem like a very small amount to be spending more each year, but given enough time it has a huge impact.

Set your Retirement Goals

Start by listing thirty retirement goals on a sheet of paper. The suggested number is thirty because the first ten are easy to identify, the next ten is somewhat harder to recognize, and the last ten makes you discover your inner dreams and passion that you have kept well inside you for several decades. Arrange your goals into short, medium and long-term goals. Assign a certain amount to each goal/your wish-list things where appropriate.

Assess your Current Financial Position

To help you achieve your retirement goals, you need to know for sure of where you are today. A net worth statement of liquid and solid cash will identify all of the assets from which retirement income may be derived.

You must also assess your retirement budget needs. What do you spend to support your current lifestyle? You may need at least 80 to 90% of your pre-retirement income to meet your goals in retirement. Preparing a retirement cash flow statement (budget) is a very important and critical task. That must be undertaken with care and at your earliest.

Identify Retirement Income Sources

Retirement income may come from a variety of sources and the percentage of each adding into your bank statement may change over time. These sources may include a pension, savings, and even part-time work. The after-tax benefit of each source of income needs to be considered. The timing of when to use each source also needs to be pre-determined.

Evaluate Retirement Risks

You must consider the risks that affect your retirement income. Inflation will erode the purchasing power of your income over time. The various investment markets/funds may occasionally falter. You may well live to be 100 years old. All of these risks need to be taken into account. Some of the risks may be known and some might some of them you might be completely oblivious too, so prepare yourself to handle the risks that you might have to face.

Assess Risk Tolerance vs. Investment Goals

Whether it’s you or a professional investment manager who is in charge of the investment decisions that you make and guides you through it, a proper portfolio allocation that balances the concerns of risk aversion and returns objectives is the most important step in retirement planning.

How much risk are you willing to take to meet your objectives? Should some income be set aside in risk-free Treasury bonds for required expenditures? So that it is saved even though your other funds are affected by the downhill economy or certain stocks you have invested into.

You need to make sure that you are comfortable with the risks being taken in your investment portfolio and know what is necessary and what luxury is. This is something that should be seriously talked about not only with your financial advisor but also with your family members.

It’s kind of like parenting: The child that needs your love the most often deserves it the least. Portfolios are similar. The mutual fund you are unhappy with this year maybe next year’s best performer so don’t bail out on it.

“Markets will go through long cycles of up and down and, if you are investing money you won’t need to touch for 40 years, you can afford to see your portfolio value rise and fall with those cycles,” said by John R. Frye.

CFA, chief investment officer, Calif said “When the market declines, but don’t sell. Refuse to give in to panic. If shirts went on sale, 20% off, you’d want to buy, right? Why not stocks if they went on sale 20% off?”

Understand Health Care Issues

Retirement usually brings a change in health care insurance coverage. when you retire you need to look for a proper health plan for your needs, as biology with age brings you multiple health-related issues for which you may and should need to secure health insurance on your own. You can find your desire plan at Jubilee General Insurance under the category of “Parents Care” plan that also covers your pre-existing medical health issues.

Long term care insurance proposals often present a confusing array of choices. How do you determine if it is right for you? Not everyone needs it. A careful evaluation of your situation is required. You can consult Smartchoice.pk for smart decisions which help you save money as well!

Invest your Retirement Assets

With goals identified and defined, develop a written investment policy that will govern your investment approach. Make your investments road map. An asset allocation (the mix of stock, bonds and cash) should be clearly stated.

The policy should also provide diversity and security of investments, be appropriate for your goals and time frame, and be in line with your risk tolerance. Within the various retirement sources, understanding the attractiveness of the asset is important, also always take into account the tax consequences of asset purchases and sales.

Manage your Retirement Income

Working in the world, we are accustomed to getting income from our employer or our business. With the onset of retirement, however, the paycheck ceases. Now income has to come from several different sources as you cannot ensure a fixed percentage of money from a permanent source all the time. Properly managing these retirement income sources requires planning and monitoring.

Monitor your Retirement Assets

It is important to conduct periodic reviews of your financial situation by monitoring your savings and your cash inflow; you can assure yourself that you will have sufficient assets to fully fund your retirement. At worst, you may discover that you may need to engage in part-time work during retirement. You need to maintain a sustainable withdrawal rate strategy.

You’re monitoring your funds reviewing it time to time with your investment expert or your family members will give you the confidence to live the retirement lifestyle that you planned.

Conclusion:

The Bottom Line os that the burden of retirement planning is falling on individuals now more than ever. Few employees can count on an employer-provided defined-benefit pension, especially in the private sector.

These steps provide general guidelines on the procedures required to improve your chances of achieving financial freedom in your later years.

One of the most challenging aspects of creating a comprehensive retirement plan lies in striking a balance between realistic return expectations and a desired standard of living. The best solution is to focus on creating a flexible saving and investment plan which can be updated regularly to reflect changing market conditions and retirement objectives.